Credit scores have a big impact on our financial lives. They affect our ability to get loans and credit cards and even influence major decisions like buying a home or getting a good job.

Think of your credit score as your financial report card. It quietly tells lenders and creditors how responsible you are with cash flow. It can get you lower interest rates on loans, make it easier to rent an apartment, and even help you negotiate better insurance prices.

On the flip side, a low credit score can create problems. It can mean higher costs when you borrow money, fewer options for credit, and more financial stress. In this article, we’ll explore credit scores, how to make them better, and how having good credit can make your financial future more secure.

The Importance of Good Credit

Good credit is like the foundation of a sturdy financial house. It’s not just about getting credit cards or loans; it affects your overall financial life in many ways.

Credit scores are super important because they open doors to financial opportunities. When you want to borrow money, lenders check your credit score to decide if they’ll lend to you and at what interest rate. If your score is high, you get lower interest rates and more chances of getting approved. This makes big purchases like homes and cars more affordable. It can also get you better credit card deals with lower interest and more rewards. But if your score is low, it can be hard to get these opportunities, and you might end up paying more.

And here’s the cool part: good credit isn’t just about borrowing money. It’s about being financially responsible and disciplined. It helps you handle life’s money challenges better, like emergencies, and save for the future. So, it’s not just a number; it’s a key to financial success and a secure future.

Building and Maintaining Good Credit

You can have good credit without taking risks like getting more credit cards or loans. It’s all about being smart with your money.

One of the most important things is to always pay your monthly payments on time. Paying your rent, utilities, and other regular expenses on time shows that you’re responsible with money. This makes your credit score better.

Also, keep an eye on your credit report to make sure it’s correct. Look at your personal information, like your name and address, to make sure it’s right. Then, check your credit accounts, like loans and credit card balances, to see if they’re accurate. If you find any mistakes, tell the credit reporting agencies to fix them so they don’t hurt your score.

Another thing is to not use too much of your credit limit. It’s generally recommended to keep your credit utilisation rate below 30% of your available credit limit. For example, if your total credit limit across all credit cards is $50,000, aim to use no more than $15,000 in credit at any given time. Keeping your utilisation low signals responsible credit management to creditors and can positively influence your credit score.

Lastly, be careful with your old credit accounts. Don’t close them, because they help your credit history look good. Just use them wisely by keeping balances low and paying on time.

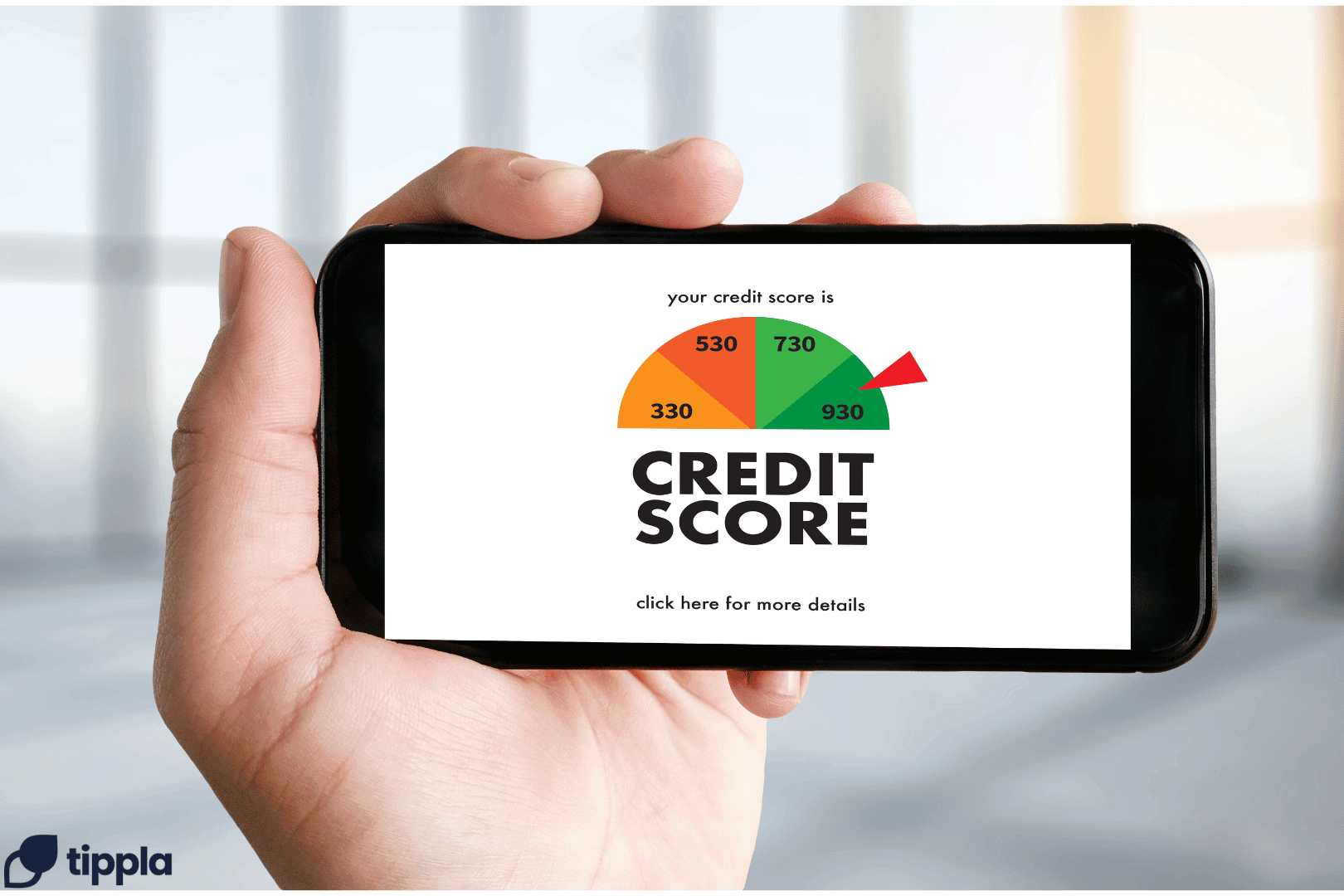

Checking Your Credit Report

Checking your credit report is like giving your financial situation and health a check-up in Australia. Here’s how to do it for free, check if it’s correct, and fix any mistakes.

You can get a free credit report in Australia from three big credit agencies: Equifax, Experian, and Illion. They have to give you a free copy of your credit report once a year. You can ask for it online through their websites, which makes it easy. Just give them the right personal information to verify your identity. You can also check your credit report on Tippla.

When you get your credit report, look at it closely to make sure everything’s right. Check your details like your name, address, and date of birth. Then, go through your financial stuff, like loans, and see if it’s correct. Look for anything that doesn’t look right, like mistakes or things that could hurt your credit score.

If you find mistakes in your credit report, it’s important to fix them. Contact the credit agency that has the wrong information and show them proof that it’s a mistake. They have to look into it and fix it within 30 days. Checking your credit report regularly and fixing mistakes can help keep your financial reputation good and your credit score high.

Using Good Credit in Financial Planning

Good credit helps you do lots of financial stuff more easily. It’s not just about getting credit cards or loans; it’s about making your whole financial plan better.

One of the best things about having good credit is that it can get you lower interest rates on loans. When your credit score is high, lenders think you’re not risky, meaning they are able to offer loans with lower interest. This means you pay less over time for things like cars or homes. Good credit can also give you more choices and flexibility when you borrow money.

Using your credit score in your big financial plan is a smart move. It’s not just about having a high score; it’s about knowing how to use it for good decisions. From managing your debts to finding good investment chances, knowing how credit fits into your financial picture helps you be more secure in the long run.

Emergency Funds and Credit

An emergency fund is crucial for covering unforeseen expenses like medical bills, car repairs, or job loss. It provides financial security and serves as a safety net in case of emergencies. Good credit allows for favourable terms and lower interest rates on credit cards or personal loans, making borrowing more affordable. It also helps avoid high-interest debt during financial crises, ensuring borrowing at lower rates and preventing a potential debt spiral. This combination of financial preparedness, emergency savings, and available credit offers flexibility. Emergency funds can be used for immediate needs, while credit lines can be used for more substantial expenses or as a backup.

But here’s the thing: you need to be careful. While credit can be a lifesaver in emergencies, it’s not the only solution. It’s really important to have money saved up in an emergency fund as your first line of defence. Depending only on credit for emergencies can lead to more money troubles later. So, having both a good emergency fund and good credit gives you a complete safety net for tough times.

Homeownership and Good Credit

Owning a home is a big deal for lots of Australians. Good credit can help make it happen. When you want to buy a house, banks look at your credit history to decide if they’ll give you a mortgage. A strong credit score shows that you’re responsible with money, which makes banks more likely to approve your loan.

Plus, good credit can get you lower interest rates on your mortgage. Even a small interest rate drop can mean saving lots of money over the life of your loan. This makes owning a home more affordable and helps you build up equity faster. It shows how important good credit is for reaching your financial goals.

Retirement Planning and Credit Scores

Planning for retirement is a long-term thing, and good credit can play a big part. Your credit history can affect your options when it comes to retirement savings and investments. It can change the terms of loans and credit lines you use for your retirement plan, making it more effective.

One option is to invest in rental properties to generate rental income during your retirement years. To do this, you need a mortgage to purchase the properties. With good credit, you qualify for a mortgage with a lower interest rate, which translates to lower monthly payments and less interest paid over the life of the loan. This allows you to acquire properties more affordably and increases your cash flow, enhancing your retirement income.

Thinking about your credit when you plan for retirement is smart. It’s not just about having good credit; it’s about using it in the right way. From getting loans for property investments to managing credit lines for business ideas, knowing how credit fits into retirement planning can open up new chances for financial growth and stability. It shows how good credit stays with you through all stages of your financial journey.

Conclusion

Good credit is a foundational pillar of sound financial planning, offering a multitude of benefits throughout life’s financial journey. It enables access to essential financial products, unlocks favourable interest rates, and enhances financial flexibility. Beyond day-to-day financial transactions, good credit also plays a pivotal role in key life milestones, from homeownership to retirement planning. It serves as both a powerful tool and a strategic asset, demonstrating the enduring impact of responsible credit management on achieving long-term financial security and prosperity.