Published in May 29, 2026

How Can You Improve Your Credit Score? A Quick Guide

We’ve said it time and again – your credit score is an important number. The higher your number, the better. A good credit score can open up many financial opportunities for you. So how can you improve your credit score? We’ve put together a quick guide to help you fix your credit score.

What is a perfect credit score?

We often get asked this question here at Tippla: what is a perfect credit score? When it comes to your score, which is also referred to as a credit rating, there’s no such thing as perfect. However, there is good – which is what everyone should be aiming for or higher.

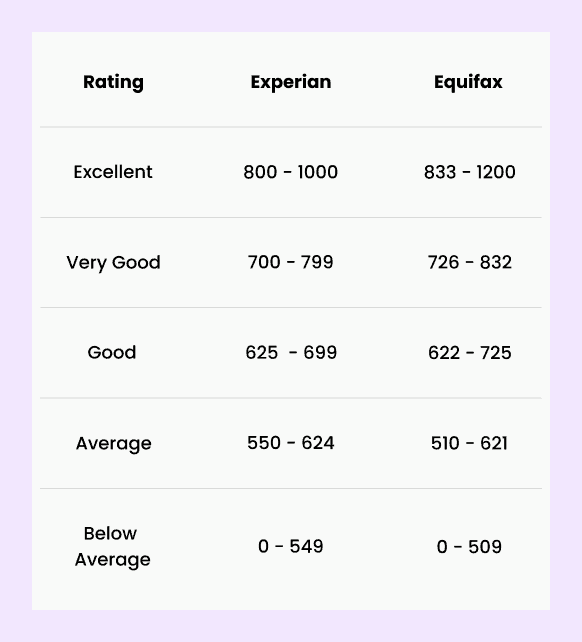

In Australia, there are three credit reporting agencies – Equifax, Experian and Illion. Therefore, Aussies don’t have just one but three credit scores. It’s highly likely that your credit score will differ across the agencies, as they have different scoring methods and scales.

Broadly speaking, your credit score is a number ranging from 0 – 1,200. Depending on your rating, it falls somewhere on a five-point scale: excellent, very good, good, average and below average.

What is a good credit score for Australia? Here’s how Equifax and Experian rank credit scores.

Source: Experian and Equifax

When it comes to credit ratings, what is a bad credit score? We think it’s important to emphasise here that your credit score isn’t a reflection of you as a person, but an indicator of how you have managed your debt in the past. If your credit score is below average or average, then there is room for improvement. That’s why we’re here – to help you improve your credit rating through understanding and healthy financial habits!

How to improve your credit score

Now you know what a good credit score is, how can you improve your credit score so that yours is good or higher? Firstly, you need to know what goes onto your credit report and what matters when it comes to your credit rating.

Your credit score is the overall number that indicates how creditworthy you are to credit providers and lenders. Your credit report, on the other hand, contains all the information that your credit score is based on.

You have a credit report for each credit score you have. In Australia you have three credit ratings, therefore, you also have three credit reports. Just as your credit ratings vary across the different bureaus, so do your credit reports. Also, you might find that you have different information on each of your reports.

Just because your information varies across your reports, doesn’t mean the information is wrong. However, 1 out of 5 credit reports contain at least one mistake that can cause your number to drop. That’s why it’s important to check your information thoroughly and frequently.

So what exactly goes onto your credit report? Your credit report contains a mix of information about your previous financial behaviours. This includes:

- Credit Accounts;

- Repayment History;

- Defaults;

- Credit Applications;

- Bankruptcies and Debt Agreements;

- Credit Report Requests.

With this in mind, how can you increase your credit score? We’ve put together a number of things you can do to fix your credit score. Tippla also recently covered a number of credit score FAQs which you might find useful.

Space out your credit applications

When you apply for a loan, a credit card, or even sign up with a new electricity supplier, this is referred to as a credit application. If you’re successful in receiving whatever type of credit you have applied for, then your application has been approved.

A lot of people don’t know this, but if you make multiple applications in a short period of time, this can actually harm your credit score. Why? Well, when you apply for credit, your creditor will assess your application and how big the risk is that you may miss a repayment or won’t be able to pay back your loan at all. Your credit report is one of the elements used to assess if you are a high or low-risk candidate.

When a credit provider does this, it is called a hard enquiry. As outlined by Equifax, “Hard inquiries serve as a timeline of when you have applied for new credit and may stay on your credit report for two years, although they typically only affect your credit scores for one year.”

The tricky thing here is, it doesn’t matter what the reality of the situation is, multiple hard enquiries can look bad to potential lenders and credit providers. Whilst you might have made multiple applications for a loan because you were trying to find the best deal, to a lender, it could look like you were in a really bad financial situation and in desperate need of cash.

With this assumption at the forefront of their mind, they may be more likely to reject your application. To be safe, it’s better to know your options before you dive deep into the world of credit.

Shop around before making an application

How can you do this? You could use comparison sites to try and find the best deals or reach out to different credit providers to learn more about their offers before making an application. By shopping around and comparing your options beforehand, you may only need to make one credit application, instead of multiple. Above all, this can protect your credit score from falling too much.

If you’re reading this and feeling worried because in the past you have made multiple credit applications at once – never fear. Time can heal all credit wounds. Now that you have this piece of information, you can use it to improve your credit score going forward.

Make your repayments on time

Your credit score is a number that indicates to lenders how reliable of a borrower you are. If you have a good credit score, then that tells them that you aren’t a risky client and in the past, you’ve handled your debt well.

Paying your bills and making your credit repayments on time, therefore, could go a long way when it concerns your credit score. In fact, your repayments make up 30% of your Equifax credit score.

That means, if you lose track of your repayments and miss, or even default on one of your bills, this could be bad news for your score. Defaults can stay on your credit report for five years, which means any time you apply for credit during this period, the provider will be able to see that you defaulted in the past and that might lead to them rejecting your application.

So how can you pay your bills on time? There are a number of things you could do to ensure you don’t miss a repayment. For example, set up a budget to make sure you have enough money to cover all of your necessary expenses. You could also set up automatic payments or direct debits.

Check your credit report frequently

Another way you could improve your credit score is by frequently checking your credit reports for mistakes, as we mentioned above, or for credit card fraud. Your credit report outlines all of the credit accounts you currently have or have had in the past two years. If you see one on your report that doesn’t belong, then you might have been subject to credit card fraud.

Discovering this early could make a lot of difference, and it’s just one of the many ways you can use your credit report for good!

Not only is it a good idea to check your report frequently in case there are any mistakes on it, it could also be useful to be familiar with your report. The more you understand your credit report and what goes into it, the more likely you’ll notice changes on your report, and whether they are good or bad.

Over time, this could give you a deeper understanding of your credit report, helping you learn which of your behaviours adversely affect your score. You can use this knowledge to avoid this behaviour and improve your credit score.

Keep your credit accounts open

You might be surprised to learn that the age of your credit account can contribute positively to your credit score. The older the account, the better it is for your rating, as it demonstrates that you can consistently handle a line of credit.

If you can show that you have been able to effectively manage your current or previous credit accounts, then lenders and credit providers might be more inclined to provide you with finance.

Whilst we’re not advocating that you keep multiple credit accounts open just for the sake of it, you might want to consider keeping some open and in use so credit reporting agencies have data to base your credit score on.

How to improve your credit score: time and consistency

Tippla hint: Stay consistent! Consistency is key if you want to improve your credit score. Unfortunately, there’s no quick fix to improve your credit score and it can’t be changed overnight. With that being said, you can fix your credit score. Sticking to the above suggestions could make all the difference – make your repayments on time, check your credit report often, space out your credit applications and more.

How long does it take to improve your credit score?

You can improve your credit score with time. But how much time are we talking about here? Well, there’s no set time limit for how long it will take. It completely depends on each individual situation and if there are any significant negative entries.

The good news is that even significant negative entries will age over time and get progressively less powerful. However, for most of them, it takes up to 7 years until they fully disappear.

Here’s what stays on your credit report and for how long:

- Credit accounts – any open credit accounts and accounts that have been closed in the past two years

- Credit enquiries – 5 years

- Repayment history – for 2 years

- Defaults – 5 years

- Court judgements – 5 years

- Bankruptcies – at least 5 years

- Serious credit infringements – 7 years

To help you fix your credit score, here’s a helpful article Tippla put together outlining the dos and don’ts of credit.

What are the consequences of bad credit?

If you’ve taken a look at your credit score and it’s not quite what you’re hoping for, never fear! It is possible to improve your credit score. But if you’re wondering if it’s even worth the effort, here are some of the consequences of bad credit.

- Credit applications might be rejected;

- Potentially higher interest rates;

- Insurance premiums could be more costly;

- It might make starting a business more difficult;

- Might cause obstacles to getting a phone contract.

Want to learn more?

If you’re hungry for more information, want to fix your credit score, and ready to embrace your inner finance geek, then head back to school! Learn what they didn’t teach you at school with Tippla’s Credit School – a free online short course which will guide you through the ins and outs of your credit score.

While we at Tippla will always do our best to provide you with the information you need to financially thrive, it’s important to note that we’re not debt counsellors, nor do we provide financial advice. Be sure to speak to your financial services professional before making any decisions.

Related articles

7 Smart Ways to Manage Your Finances and Save on Fees

29/05/2026

High inflation and rising operating costs are just two...

Can You Refinance Your Home Loan to Consolidate Debt?

29/05/2026

Do you want to know more about how to...

No Deposit Bonuses in Australia: How They Work, Risks & How to Claim

02/06/2026

No Deposit Bonuses for Australians – Are They Worth...

Wonaco casino cz – platební metody a rychlost výběrů

02/06/2026

Registrace a první kroky Jak se zaregistrovat krok po...

Subscribe to our newsletter

Stay up to date with Tippla's financial blog