Published in July 18, 2023

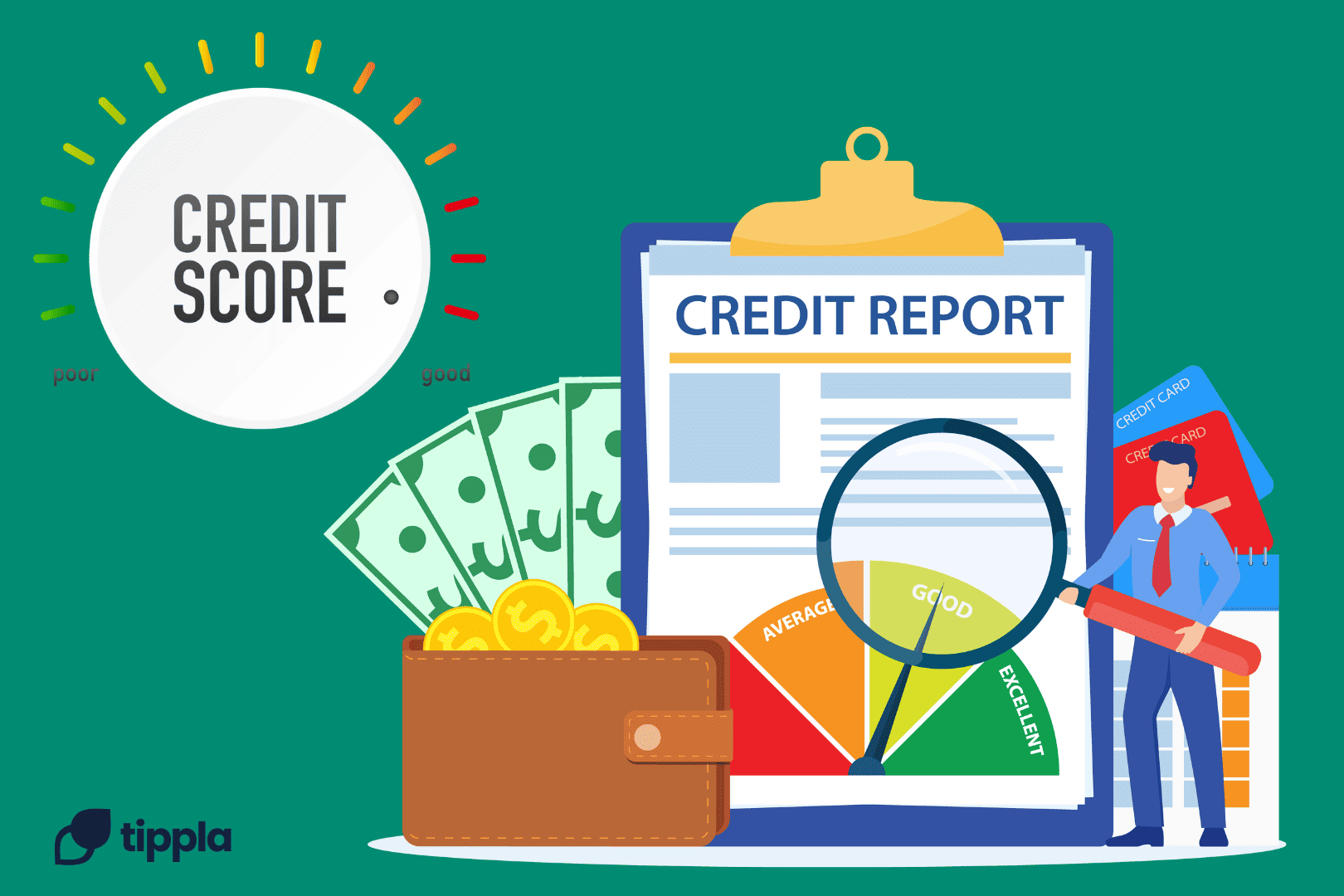

How to Understand Your Experian Score

The key to your financial development

The fact is, unless you’re the heir to a healthy trust fund or the winner of a million-dollar lottery, there are certain things in life that you simply can’t afford to pay for upfront. Things like a home, a car, and an education just don’t come cheap. So, chances are there will come a time when you find yourself needing to borrow money.

Lending money or offering credit is a game of risk for banks and financial institutions. They need to know how likely a borrower is to pay that money back. To do this they employ credit reporting agencies, who offer up a simple number of three or four digits called a credit score.

A credit score is basically a borrower’s risk to a lender, represented in a number. While it’s not the only factor that a lender will take into consideration when determining whether a loan or credit card application is accepted, it’s often the defining one. Understanding your credit score can consequently give you the power to improve it and your overall financial position.

But in spite of its importance, most people don’t really understand their score – what it is, why it matters, and how it came to be. So today we’ll be looking at everything you need to know about your Experian score. That is, the number generated by one of Australia’s three major credit reporting agencies (the others being Equifax and illion).

What do you need to know about your Experian score, and how do you get it working for you rather than against you? Let’s take a look.

Experian credit scores 101

Credit scores are designed to represent the financial responsibility of an individual and the risk they represent to a lender – in a number. After an individual’s financial history has been analysed, a number is assigned that ‘predicts’ the likely outcome of a loan or credit card over the next 12 months. So, whether repayments will be made or missed, whether a loan will go into default, or whether something more serious like bankruptcy will occur. That’s quite a lot for one single number.

Based in Ireland, Experian is one of the largest credit reporting agencies in the world, collecting and analysing the financial information of over one billion people worldwide. An Experian credit score is given on a scale of 0 to 1000 – zero being the worst possible score and 1000 being the best.

While your score will play a key role in whether a loan or credit card application is approved, it’s important to note that isn’t the only factor at play. Your relationship with the lender and other pieces of the puzzle will also be considered.

Key contributing factors

So, what do Experian look at when calculating your credit score? According to the agency itself, the score is based on the following five factors:

- Payment history: How faithful are you with your repayments, whether they’re on a loan or for a credit card? Lenders want to be confident that they can trust you to repay your debts on time, so even one missed repayment will have a negative effect on your score. According to Experian, this is the most heavily-weighted factor, accounting for as much as 35% of your score.

- Credit utilisation: Another major factor in creating your credit score, accounting for up to 30% of the final number, is your credit utilisation ratio. This is calculated by looking at the ratio of credit card balances to credit card limits, and the ratio of loan balances to the original loan amounts. The less credit you’re utilising, and the faster you pay down your loan debt, the better your score will be.

- Credit mix: A lender wants to see that you are capable of handling different types of debt, be it in instalment accounts (loans), revolving accounts (credit cards), or for a variety of different assets – a home or a car, for example. The greater the mix, the better the score, provided it is all regularly repaid of course.

- Hard enquiries: Whenever you submit a loan or credit card application a lender will request your credit report, and these ‘hard enquiries’ are logged in your credit file. Too many enquiries can negatively affect your credit score, as this can be a sign that you are desperately trying to obtain credit (and failing).

- Negative information: Late payments, missed payments, charge-offs, collection accounts, foreclosures, bankruptcies; all of these events are logged in your credit file, and represent red flags to lenders. The degree to which negative information affects your score will depend on the information itself. If it’s something minor like a late payment, its influence will be low. If it’s something major, like bankruptcy, it could devastate your score.

Why does my Experian score change?

You can see that there are plenty of reasons why your Experian score might change, be they for better or for worse. But some of the most common reasons your score might go up or down include:

- Cancelling a credit card or paying off a loan: Paying off debt or reducing your financial exposure will generally improve your credit score.

- Paying a bill or making a repayment late: Not making a payment on time, whether it’s for a credit card instalment, loan repayment, or even phone or utility bill, is perhaps the most common way that credit scores are negatively affected.

- Submitting a loan/credit card application: If a number of hard enquiries are logged on your file in a short amount of time, it will negatively affect your score. You should only ever apply for one credit card or loan at a time. A recently denied application will also have a negative effect. On the flipside, an approved application will have a positive effect on your score.

- Making changes to your loan/credit limit: Any change to your current financial arrangements, be it to a credit card, a loan or otherwise, could result in a change in your score.

- New information is added to your file: Experian has to source all of its data from credit providers, and sometimes those providers take their sweet time in passing that data on. This can see your credit score changing even in periods when you’re not financially active.

- Old information is removed from your file: At the other end of the process, all data has an expiration date. When this data is removed from your credit report it can either affect your score positively (if it was negative data) or negatively (if it was positive data).

How often does my Experian score get updated?

In short: all the time! New information is constantly added and removed from your credit file, so your credit score could hypothetically change every time you check it, even if it’s the next day.

That said, most of the data on your credit report is updated monthly, so it’s likely that you’ll see minimal change in your score day-to-day, but may see change from month-to-month. This ‘data dump’ usually happens at the beginning of a new month, so aim to check your score at this time if you’re looking for a current and relatively stable measure.

The key differences between your ‘report’ and ‘score’

Because many of us will only think about our Experian score a handful of times in our lives, a few of the terms that are used might be a little confusing. First of all this number might be described as either a ‘credit score’ or ‘credit rating’ – there’s no difference. In Australia at least, these two terms mean the exact same thing. True to form, we just like to talk in riddles here.

Slightly more confusing is the difference between a credit report and a credit score. These two things essentially offer up the same information, but in different forms.

- A credit report is a full overview of your finances, displaying any information relevant to your ability to manage debt and credit.

- A credit score represents all of the information in your credit report in a single, simple number, which in the case of an Experian score is between 0 and 1000.

What do the different score ranges mean?

So your Experian score is a number between 0 (the worst possible) and 1000 (the best possible). But what does it mean to fall in between? Let’s take a look at how Experian define their score ranges.

| Rating | Score | Reasoning |

| Excellent | 800 – 1000 | Your score is well above the Experian average. It is highly unlikely that you’ll experience financial difficulties in the near future, and you’re almost guaranteed to secure credit or gain approval on loans. |

| Very Good | 700 – 799 | Your score is above the Experian average. It is unlikely that you’ll experience financial difficulties in the near future, and you should have no problem securing credit or gaining approval on loans. |

| Good | 625 – 699 | Your score is around the Experian average. There is a chance – albeit small – that you’ll experience financial difficulties in the near future, so lenders will be more careful when assessing your applications. |

| Average | 550 – 624 | Your score is below the Experian average. It is somewhat likely that you’ll experience financial difficulties in the near future, so it may be more difficult for you to secure credit or gain approval on loans. |

| Below Average | 0 – 549 | Your score is well below the Experian average. It is likely that you’ll experience financial difficulties in the near future, so it will be difficult for you to secure credit or gain approval on loans. |

I don’t have an Experian score – should I be worried?

A score of zero and no score are two very different things. In order to create their score, Experian has to evaluate your credit and debt history. If you don’t have a history, you won’t have a score.

Most lenders require a borrower to have some form of credit history before they will be willing to approve a credit or loan application. So, you’ll need to put something like a mobile phone plan or a utility bill in your name if you want to generate an Experian score.

If you’re anything like the rest of us, you haven’t won the Powerball or inherited a 40-acre estate. You’ll therefore need to access credit or go into debt in order to make those investments that are so important in life – the house, the car, the education. Because while the words ‘debt’ and ‘credit’ can come with some not-so-sexy connotations, the truth is that they are the most important financial tools at your disposal, allowing you to strengthen your position in a way that your own money never could.

The key to accessing these tools is a simple number between 0 and 1000. And by understanding that number, you’ll be able to get it working for you, not against you.

Whip your credit into shape, with Tippla

Do you want to check, monitor and improve your credit score? What if we said it didn’t have to cost you anything? That’s what you get when you sign up to Tippla!

Sign up to Tippla and let us help you reach your financial goals with our smart monitoring and insights. We compare your score from multiple reporting agencies to give you the best understanding of your credit.

For smarter credit checks, choose Tippla.

While we at Tippla will always do our best to provide you with the information you need to financially thrive, it’s important to note that we’re not debt counsellors, nor do we provide financial advice. Be sure to speak to your financial services professional before making any decisions.

While we at Tippla will always do our best to provide you with the information you need to financially thrive, it’s important to note that we’re not debt counsellors, nor do we provide financial advice. Be sure to speak to your financial services professional before making any decisions.

Related articles

How to Reduce the Interest on Your Home Loan

29/07/2021

When you take out a loan, you’re not only...

Credit Scores vs Credit Reports: Understanding the Difference in Australia

23/10/2023

Understanding the nuances of credit scores and credit reports...

How to Report Credit Card Fraud: Protect Yourself and Your Credit Score

26/07/2021

Fraudsters are adopting more sophisticated methods to steal your...

Credit Enquiries for Auto Loans

24/11/2023

Undergoing the Car Financing Process Without Harming Your Credit...

Subscribe to our newsletter

Stay up to date with Tippla's financial blog